We all have them. Those apps we open without thinking. Not because we need anything in particular, but because they feel… safe, in some…

10 tips on how to raise venture capital in South Africa [Opinion]

Entrepreneurs constantly disrupt the balance of competition by unlocking inventive commercial opportunities and creating new markets in doing so.

This can sometimes be done by bootstrapping (with minimal financial resources) over time, but because of the rapidly changing environment innovation-driven entrepreneurs operate in, some form of risk funding is usually required to scale viable opportunities. Raising venture capital (VC) is one way to do it.

VC firms invest in early-stage, emerging small firms with high growth potential in exchange for minority equity ownership. But for many SA startups and small businesses, this remains theoretical.

While VC is a recognised alternative asset class in many countries, it is still an emerging industry in SA with few (but increasing) VCs around that have limited funds to deploy. Local entrepreneurs seeking risk funding should therefore get resourceful to increase their VC funding chances…

Here’s how VCs can do it:

1) VC backable scalable business model?

Venture capital should not be the go-to funding choice for everyone starting a business. A startup is a high growth potential company in search of a repeatable and scalable business model. Once it gets product or market fit and some traction through the scale-up phase it turns into a so-called “gazelle” – an extremely fast-growing company (not measured off a low base), which maintains consistent expansion of revenue, employment or profit metrics over a prolonged period of time. If your business model does not fit within the spectrum of these definitions it is not VC backable and other funding mechanisms may be more appropriate.

2) Target an investor universe

VC investors will do a thorough due diligence on you, your business and the growth assumptions behind it. Start by turning the tables on them. Do your homework on who the active and credible investors in the market are. Talk to their current or past portfolio companies. Study their investment mandates and make sure you are a good fit for each other. Southern Africa Venture Capital and Private Equity Association (Savca) members and the list of the SA Revenue Service’s (Sars) Section 12J VCCs could help, and increasingly international VCs are turning their sights to Africa so look out for those.

3) Get Referred

It is not necessarily a well-known fact that most VC deals originate via leads passed on from within the wider trusted networks of the VC community. Use the concept of six degrees of separation to find a way to get introduced. Or trawl the startup scene for networking events. A warm referral to a VC goes a long way to securing that first meeting.

4) Refine Your Elevator Pitch

You need to be able to convince a VC that your Startup is worth investing in by communicating all of the core elements of your venture in a clear and concise manner. Define your company’s purpose, perfect your one-line pitch and strive to tell a four-word story. Then let your inner circle of friends and mentors know what you are up to.

5) One-page teaser doc

Startups should always have a clinical “one-pager” summary of their business and the investment requirements on hand. Mainly used to immediately follow up when your elevator pitch worked and a potential funder or partner says: “Sounds interesting, can you send me some more info?”. Also makes it easier and more professional when your referral network does an intro by leading with this one-pager.

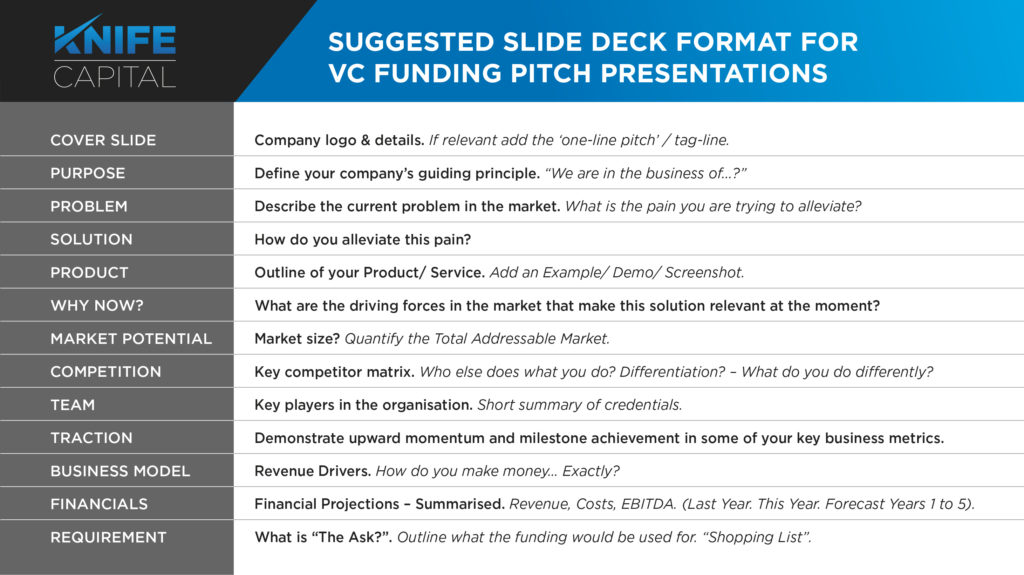

6) Standard Pitch Deck

Yes — we know some entrepreneurs have their own ideas of what information potential VC funders would like to see (keep that on hand for the due diligence data room), but why not just use the tried and tested pitch deck format that is used the world over for the first meeting with a VC that goes something like:

7) Granular financial model

Like it or not, at some level all roads lead to the assumptions behind your financial model. VC’s have heard it all from the ever-present “these projections are conservative” to “real life won’t mimic excel anyway so what’s the point of building a model”. Build a model. And make it granular. We know there will be pivots, delays, underestimation of costs, corporates who pay late and unexpected windfalls. But we need to agree on the basic set of metrics that reflect the commercial DNA of the business. At this snapshot in time.

8) Due diligence data room

A data room is a place where the startup or small business places copies of the financial, legal and business documents that define the history and future of the company. It can be physical, virtual or a combination thereof and is accessed by potential investors during due diligence — usually after having signed a “non-disclosure agreement”. Keep it updated before approaching VC investors as two things happen in an investor’s mind when a startup says: “I can give you access to my virtual data room”… One: they know that this entrepreneurial team has got their act together and managing the partnership post-investment will be a pleasure; and two: there is a perceived sense of urgency as other investors may already be analysing the information. Have a limited data room ready with just the key information that you are willing to share and then also a comprehensive one for when negotiations heat up.

9) Push for term sheet

Real VCs are in the business to invest. If you don’t get a term sheet or letter of intent from a VC to invest within a reasonable timeframe something is wrong. This could be mainly one of two things: For various reasons there is no real interest from the VC and you are in the “slow maybe” pile; or you have not enabled the VC with enough relevant information to make a “yes or no” decision. Figure out which it is. Respond timeously to information requests. Push for a decision either way. If needs be, work through the person that referred you to the VC in the first place.

10) Avoid deal fatigue in due diligence finalisation and legal closing

This post is not about the intricacies of the due diligence process or legal negotiation tips. But once you have “passed” the due diligence exercise there is usually a working list of things to get done as suspensive conditions to the potential transaction, and the legal closing process takes its course. Some legal tweaks are inevitable. This can be relatively painful if the spirit of partnership is not already present in the way parties negotiate with each other. Avoid so-called deal fatigue by finding sensible compromises to negotiation obstacles, meeting suspensive conditions quickly and working with the best lawyers.

… And put the Champagne on ice!

Keet van Zyl is a partner at South African venture capital fund Knife Capital. This article first appeared on Medium. See the original one here.

Featured image: moritz320 via Pixabay